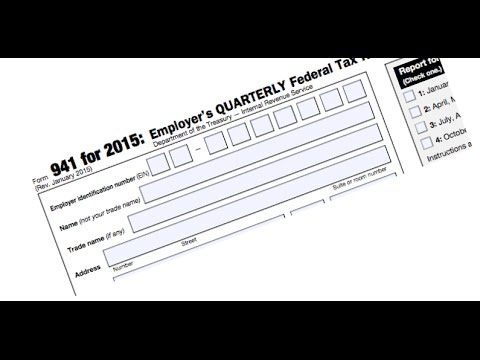

Hi, I'm Cynthia Cox with Cox and Associates CPAs LLC, and this is the Nonprofit Minute. Today, I want to discuss an issue I often see with organizations that have both ministerial employees and regular employees. When filing their 941 forms, they encounter different challenges due to this mix of employees. So, how do you handle the situation when you have ministers who receive a housing allowance? Well, the housing allowance is not subject to federal income tax but is subject to self-employment tax. Therefore, on the 941 form, you need to subtract the housing allowance from the total wages. All other compensation or wages, apart from the housing allowance, should be reported on line two as wages, tips, and other compensation. Line three is where you report the total federal income tax withheld from these wages. We discussed voluntary withholding in a previous YouTube video. For ministers, all their withholding should be recorded on line three under federal income tax withheld. Moving on, lines five A, B, and C, deal with Social Security wages. However, these lines do not include any amounts from ministers since they are self-employed and not subject to Social Security wages. It may seem counterintuitive, but that's how it works. Ministers' wages should be reported on line two and should not be included on lines five A, B, or C. Once you have filled out line five without including any ministers' wages, simply follow the instructions as you would for any other organization or company. By doing so, you will complete the 941 form without any issues. In reality, ministers do complicate things, although one may not be supposed to say that. However, those of you who work with them regularly understand what I mean. If you need assistance with these complex issues that often involve non-intuitive laws, please don't...

Award-winning PDF software

Video instructions and help with filling out and completing Form 8655 Payroll